The Learning Team | Customers, Etc.

Net present value, options, and the learning team

Let’s play a game. We’ll pretend that I’m going to give you a million dollars and you have to come up with a business model where, at the end of five years, the discounted value of future cash flows exceeds the million dollars originally invested in the project.

“Do I have to create something of value for customers?”

Customers? Come on. We’re doing finance. Just the numbers, please.

“Uh, sure, okay. I’ll take your initial million dollar investment, make a product, and then sell that product such that we make a $250,000 profit per year for 5 years. You gave us a million dollars. We returned to you $1.25 million.”

Investment -$ 1,000,000

Year 1 $ 250,000

Year 2 $ 250,000

Year 3 $ 250,000

Year 4 $ 250,000

Year 5 $ 250,000

=========================

NPV $ 1,250,000

Okay, that’s cool, but if I had invested my money in the stock market, I would have expected a 10% return on my money. Money received in the future isn’t value as money in my pocket now, so when you discount your cash flows, the net present value (NPV) of you business ends up being negative.

Investment -$ 1,000,000

Year 1 $ 250,000 / 1.1^1 = $227,273

Year 2 $ 250,000 / 1.1^2 = $206,612

Year 3 $ 250,000 / 1.1^3 = $187,829

Year 4 $ 250,000 / 1.1^4 = $170,753

Year 5 $ 250,000 / 1.1^5 = $155,230

============================================

NPV -$ 52,303

With a negative NPV, I should have just invested in the stock market.

“Okay, fine, the business will make $500,000 profit per year. I think we can both agree that’s a good investment.”

Investment -$ 1,000,000

Year 1 $ 500,000 / 1.1^1 = $454,545

Year 2 $ 500,000 / 1.1^2 = $413,223

Year 3 $ 500,000 / 1.1^3 = $375,657

Year 4 $ 500,000 / 1.1^4 = $341,507

Year 5 $ 500,000 / 1.1^5 = $310,461

=================================================

NPV $ 895,393

Yes, fine, the math works out. But your business is risky. It doesn’t even have customers!

“You told me not to worry about customers!”

This is finance. Let’s be serious. Of course we have to worry about customers. Anyway, your business is risky. What are the odds that your business fails?

“My totally fake business that doesn’t have any customers?”

Yeah, that one.

“Fifty Percent.”

Year 1 $ 500,000 / 1.1^1 * .5 = $227,273

Year 2 $ 500,000 / 1.1^2 * .5 = $206,612

Year 3 $ 500,000 / 1.1^3 * .5 = $187,829

Year 4 $ 500,000 / 1.1^4 * .5 = $170,753

Year 5 $ 500,000 / 1.1^5 * .5 = $155,230

=================================================

TOTAL $ 947,697

We’re right back where we started. When we consider the odds of failure at 50% and subtract my initial $1 million investment, the net present value of my investment is still negative, -$52,303.

“Okay, but we should know after the end of the first year if our project is a success or not. If it’s not generating cash after the first year, we’ll return $500,000 of the cash back to you.”

Year 1 $ 0

Year 2 $ 500,000 / 1.1^2 * .5 = $206,612

Year 3 $ 0

Year 4 $ 0

Year 5 $ 0

=================================================

TOTAL $ 206,612

You make a good point. When we add the two options together and subtract the initial investment, the total NPV is positive.

Investment -$ 1,000,000

NPV Option 1 $ 947,697

NPV Option 2 $ 206,612

=========================

TOTAL NPV $ 154,308

I’m feeling better about my investment, but could you fail… faster?

“You mean, take bigger bets, but try to learn as quickly as possible if they’re successful so we can pivot to try something new?”

Yes, exactly.

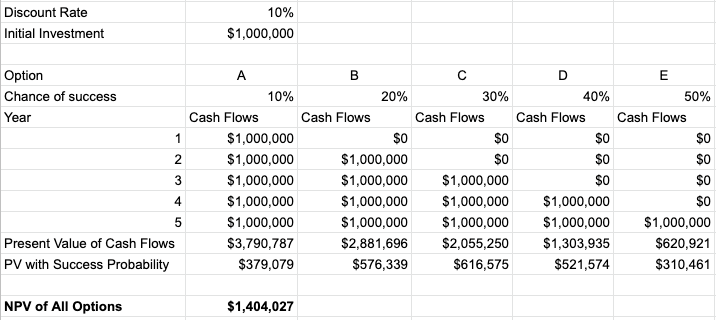

“Okay, we’re going to try to make a million dollars per year, but this is a big bet, so there’s only a 10% chance that we’ll succeed in the first year. If we fail, we’ll try again the next year, but this time we’ll have learned from our mistakes, so there will now be a 20% chance that we’ll succeed. We’ll keep trying, failing, and learning, such that by the last year there will be a 50% probability that we’re successful at generating a million dollars in cash flows.”

When we add up the present value of all discounted cashflows, consider their probability of success, and subtract the initial million dollar investment, the net present value comes out to be $1,404,027. We should consider investing in this learning organization.

Options have value

One of the things you pick up on in business school is how many examples in both finance and accounting have their origin in the world of manufacturing. You get stories like what we have above, but in reference to buying property and equipment: “You’re considering making a $1,000,000 investment in a machine that will generate cash flows of $250,000 per year for 5 years.”

It’s a straightforward scenario, and when you factor in the time value of money and the probability of failure, you start wondering why you’re investing in a machine.

Things start to get interesting when you add options. Options have value. They cannot be negative. “If the business looks like a failure after the first year, you’ll have the option to sell the machine for $500,000 and return money to your investors by the end of the second year.” The value of the option can make an otherwise risky investment start to make sense.

If options always have value, that means that if you can increase the frequency of options for success, your initial investment is more likely to pay off.

Teams invite optionality

The thing about investing in machines is that they’re really only “hired” to do one thing. You can salvage a machine and sell it at a discount, but you’re not going to be able to re-invest in another machine of equal price without acquiring more capital.

Humans, on the other hand, are different. We learn and adapt. We have the ability to experiment. Put another way, we generate options. The faster we are able to experiment and move on to a new opportunity to create value, the greater the possibility of long-term success.

Speed is important

If a team spends five years coming up with a business model, only to fail at the end, the team has left itself no options. It’d be better to create a minimum-viable product, talk to prospective customers, fail quickly, learn, and try again. Each attempt generates a new option. The faster your iterations in your feedback loop, the more options you’re able to generate. Teams that fail quickly are able to incorporate their learnings into future iterations, increasing the probability of success as they increase their options.

The value of the learning team

The learning team is incredibly valuable, far more valuable than a machine. Perhaps you can salvage a machine for 50% of what you paid for it if your project fails, but if you have a team of people who are learning from their failures and able to increase the probability that they’ll generate cash flows in the future, that’s an incredible investment.

In the final example of the first section, I’m making a huge assumption, namely, that the entire team will stick around through failure after failure. If you have to hire a new team after each failure, you lose the learning of the team that gave future options a greater probability of success. In order for this model to succeed, you have to structure the organization such that learning from failure is rewarded and the learning of the team is retained within the company.

This brings me back to what we talked about a few weeks ago in regards to ownership. For teams that demonstrate an ability to fail and learn quickly and apply those learnings to the future ability to generate cash flows, giving team members ownership in the value of their team is one of the surest ways to align individual success with the success of the overall team, thus retaining knowledge within the team over the long term.

"If you have to hire a new team after each failure, you lose the learning of the team that gave future options a greater probability of success." This is also why knowledge management needs to be a key focus of any growing and experimenting company ;)